The national electricity strategy provides the vision. The Building Decarbonization Alliance is already at work on the demand-side implementation.

When Prime Minister Mark Carney committed to doubling Canada’s electricity system in the new National Strategy for an Electrified Economy, he emphasized something the Building Decarbonization Alliance has noted for some time: electrification is economic strategy, not a climate compliance exercise.

At our Forum in Ottawa last November, drawing on the work of EMBER and others, we described the world entering an electrotech era — a global economic shift as consequential as the age of steam, rail or oil. The national strategy reflects that understanding and we’re glad it has. In their response to the strategy, our colleagues at the Transition Accelerator pointed out that electrification across buildings, transportation, and industry is “the real prize”— the 74 percent of Canada’s emissions that electricity can displace and the $15B that Canadians can save in total energy costs by doubling supply.

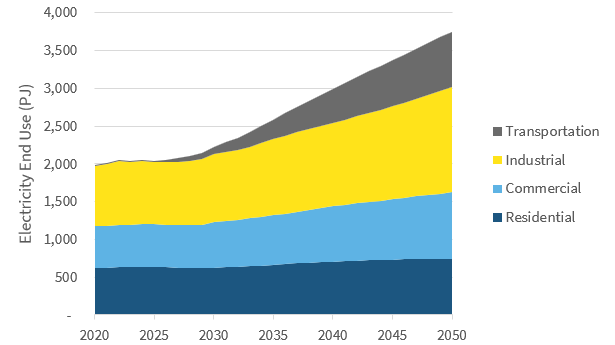

But committing to doubling supply also means answering a question the strategy only begins to address: how does Canada’s building stock — a six-trillion-dollar asset class — drive the demand for that electricity in a way that the system can respond to and that keeps it affordable and reliable? The Canadian Energy Regulator projects that residential and commercial buildings end-use electricity will grow by about 40% to 2050. That is where the demand-side question will be answered, and it is where the real work lies for the building sector.

Buildings Aren't a Problem to Solve. They're a Resource to Develop.

For far too long — about four decades — the conversation about buildings and climate has been framed as an efficiency problem. The solution for making buildings ever-more efficient rested on owners implementing deep energy efficiency retrofit projects without specific focus on the fuel source. The whole sector relied on projects justified almost exclusively by energy cost savings and utility demand-side management (DSM) incentives funded through avoided electricity or gas supply costs. On new construction, for almost two and a half decades, building codes have focused on making buildings more efficient at using whatever source of fuel they chose. This framing still dominates the sector, and it slows decarbonization progress and obscures the real opportunity associated with smart building electrification.

In our view, smart electrification is better understood as a well-timed asset renewal strategy, and a long-term new building valuation play. Hundreds of thousands of times every year, heating and cooling systems across Canada are selected for a new buildings or reach the end of their useful life and need replacement in an existing one. Every one of those moments represents a fork in the climate road: lock in another 15+ years of fossil fuel combustion, or make the better and more efficient electric technology the easier choice. When policy and incentives align around those moments, the economics improve dramatically and the transition happens at a pace the market more readily supports.

The National Strategy for an Electrified Economy is already aligned with parts of this approach — strengthening building codes and their adoption, introducing targeted demand-side measures, supporting retrofits (including heat pumps) for up to one million households, and encouraging integrated resource planning across gas, electric, and thermal networks. Organizations like the Pembina Institute are recognizing the same shift: the demand side of the meter is a system resource, not just a retrofit target.

The shift from “climate obligation” to “economic asset renewal and valuation” is the lens that makes the building transition legible to owners, lenders, and markets — not just to policy makers.

Managing the Peak: Buildings as Grid Assets, Not Grid Burdens

Without increased coordination, the transition will raise peak demand more than necessary, push up electricity rates, and weaken the affordability case for electrification (which is the outcome the strategy is designed to avoid). The difference between a managed and unmanaged transition is not marginal. It could be measured in the hundreds of billions of dollars in distribution infrastructure over the next 25 years.

How and when buildings electrify is a part of the solution. Flexible loads that shift to off-peak periods, hybrid heating strategies that electrify in step with winter-peaking grids, thermal networks that capture waste heat and put it to productive use across multiple buildings — these are the tools that make the grid work better, not harder. The transmission system moves power. The distribution system delivers the transition. And whether and how much buildings help or hurt depends entirely on whether the right frameworks are in place to optimize investments.

Thermal Energy Networks (TENs) deserve specific mention because the new strategy calls them out explicitly in its integrated resource planning commitment. TENs remain one of the most underused tools in the transition toolkit. Our TENs work, funded through The Atmospheric Fund (TAF), has shown benefits and barriers associated with TENs, and has produced a support toolkit for decisionmakers considering TENs. BDA’s federally-funded OERD research project is working now on the regulatory reforms that would allow gas utilities, electric utilities, and thermal utilities to deploy TENs at scale — producing the framework options that provincial and federal governments will need. These reforms could also propel other important new thermal energy delivery services and business models, as shown in our latest research on Geothermal-as-a-Service (GaaS).

The market is also sending signals that policy needs to follow. Our partners at Recursive Advisors and Affine Climate Solutions, drawing on their Banking on Buildings program and Value at Risk tool, have developed a compelling way to think about this. In 1887, a developer who skipped installing the elevator saved money — until every new building had one, and buildings with only stairs started losing tenants. The same dynamic played out generations later with tall warehouse ceilings in the on-line delivery boom. Electrification readiness is the new elevator or tall ceiling. For savvy building owners, the National Strategy for an Electrified Economy is a clear market signal. The future is electric. The question is whether your assets are positioned for it or not.

BDA’s work continues to focus on deploying our coalition and our modelling tools, and co-developing credible solutions to answer the critical questions: what does a managed transition actually save, who captures those savings, and which regulatory reforms make it possible?

Three Options to Build Momentum

First: an AC-to-HP policy, the lowest-friction option available in the buildings space. AC adoption is climbing fast under the Canadian summer sun: millions of units will go in over the coming decade regardless of policy, including roughly 200,000 central air conditioners reaching end of life in Canada each year. Requiring them to be able to both cool and heat just makes sense. With the 18-month lead time manufacturers have confirmed to us that they can meet, coupled with a midstream incentive to cover the small incremental cost, such a policy cost-efficiently converts the PM’s one-million-household commitment into a cost-effective, durable and low-friction market transformation. Bill S-4, which the strategy references to modernize the Energy Efficiency Act, is the enabling vehicle.

Second: renew (and improve) a heat pump incentive program. The Greener Homes loan and grant offerings proved there is real homeowner demand for heating system upgrades. A successor loan program could disburse funds as payments come due rather than leaving homeowners to front them, and it could relax homeowner credit requirement via a loan loss reserve to expand eligibility. It could also do more to blend federal funds with private capital to reach more households and explore third-party delivery agents who could originate loans. If a grant program is also envisioned, it could publish a predictable five-year declining schedule like the EV incentive, target eligibility and grant levels to protect affordability for those who need it most, and pair it with the mid-stream AC-to-HP market transformation strategy explained above. This would not require a new program; it would be a refined and more effective version of an existing commitment.

Third: signal to the financial system that climate-aligned buildings carry lower risk. Banks currently hold the same regulatory capital against a fossil-fuel-dependent building and an electrified, grid-ready one. Two decades of evidence in Canada, the U.S., and Europe shows that high-performance buildings carry lower default risk and more stable income profiles. Our BDA Partner Affine Climate Solutions, in collaboration with us and others in the financial sector, is building the case for the Office of the Superintendent of Financial Institutions (OSFI) to explore targeted capital relief for climate-aligned real estate lending — a market-based mechanism that would unlock retrofit investment at scale without a new spending program.

The Electricity Strategy Provides the Goal. Buildings Can Help Deliver It.

Much of the work to be done points to the fact that a managed transition is not a technology problem — it is a coordination problem. The building sector is not waiting for government to begin coordinating action in the sector. Our upcoming National Building Decarbonization Action Plan, developed through extensive consultation with the building ecosystem, identifies close to 100 actions that manufacturers, distributors, utilities, municipalities, lenders, and building owners can take now — many without any new government program. We will be releasing it later in 2026 as a coordination tool for the sector.

The National Strategy for an Electrified Economy tells us what to build. Buildings can either be seen as a burden — driving unmanaged peak demand and expensive infrastructure — or a support: flexible, efficient, high-value assets that help reduce peak load and deliver value to everyone connected to the grid.

Treating buildings as strategic assets, not as a compliance problem, is how we make Canada’s electricity transition work for households, communities, and the economy. That is the opportunity this strategy opens, and it is the work the BDA is here to help deliver.